|

Money

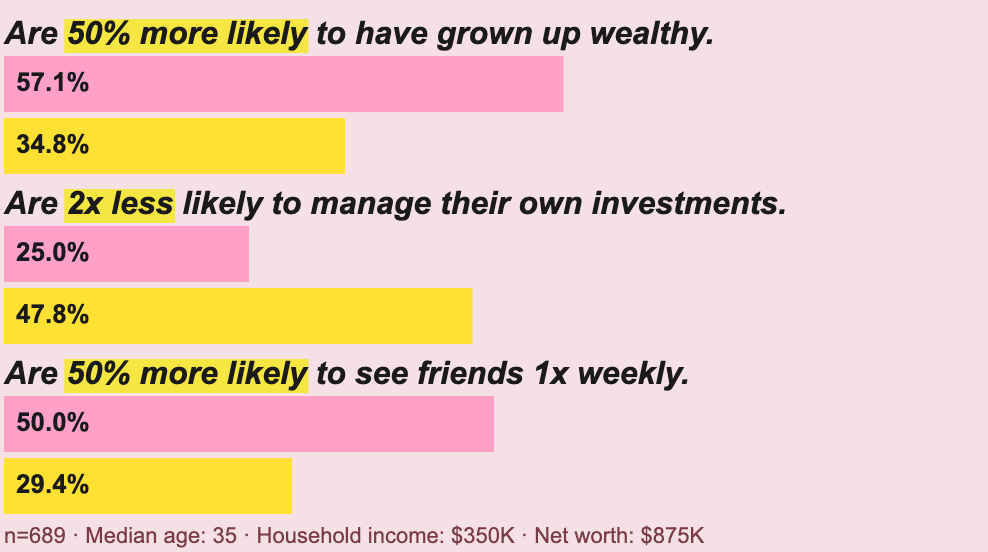

Sapphire Reserve cardholders are in a co-operative. Nobody told them.

In 1871, a group of British army and navy officers in London decided they were paying too much for their wine.

Enterprising Etonians — with military ranks purchased via the "sale of commission" system — they schemed up a solution: they would pool their money and buy wholesale. The strategy worked so well that, tipsy with success, they started buying port, stationery, Stilton and saddle soap. Within five years, their store in the heart of Westminster had added a tailoring department, a pharmacy, and a banking arm. By 1878, their profit margin was so extreme that the House of Commons convened a select committee to investigate the officers for unfair competition.

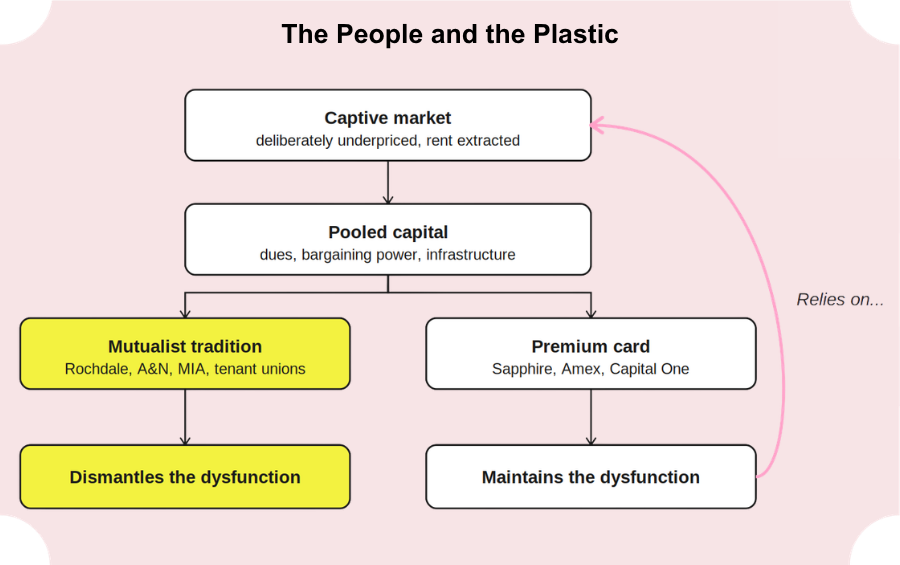

The Army & Navy Co-operative Society was the first mutualist society for the economic semi-elite. The idea had trickled up from the Civil Service Supply Association, which six years earlier had been founded by post office clerks pooling for half a chest of tea. As with other 19th-century mutualist projects — the Rochdale Pioneers, the friendly societies, the credit unions, the mutual insurance societies, the Co-operative Wholesale Society — the A&N allowed the generously pensioned to flex their collective consumer power.

A&N ceased to be a cooperative in 1934 and now persists as a department store chain, but the pooling model has not lost its popularity among the oenophilic and upwardly mobile. Last year, Chase Sapphire Reserve cardholders were invited to a private wine tasting and performance by the Philadelphia indie rock band Mt. Joy (sample lyric: we're gonna tear down these fascist clowns) held in Napa and co-sponsored by Land Rover — itself a product of the British military establishment.

Chase Sapphire Reserve and its chief competitor for points-prospectors business, American Express Platinum, are semi-mutualist efforts with the mutualism obscured. They may look like financial products, but structurally they are buying clubs: in exchange for paying dues, members benefit from group bargaining, wholesale discounts, and gated access to scarce goods. But the parallel is not totally apt. The A&N was founded to solve a problem — Bordeaux-based wine importers price-gouging members of Pall Mall clubs [3] — whereas the credit card was founded to allow JPMorgan Chase and American Express to extract profit from broken pricing systems while propping them up.

Traditional mutualist societies had politics. They agitated. Credit cards have points. They capitulate. Cardholders pay $795 a year to skip queues and to access airport lounges that exist in part because the domestic terminal of every American airport east of Denver is unbearable. The convenience business requires inconvenience to create value.

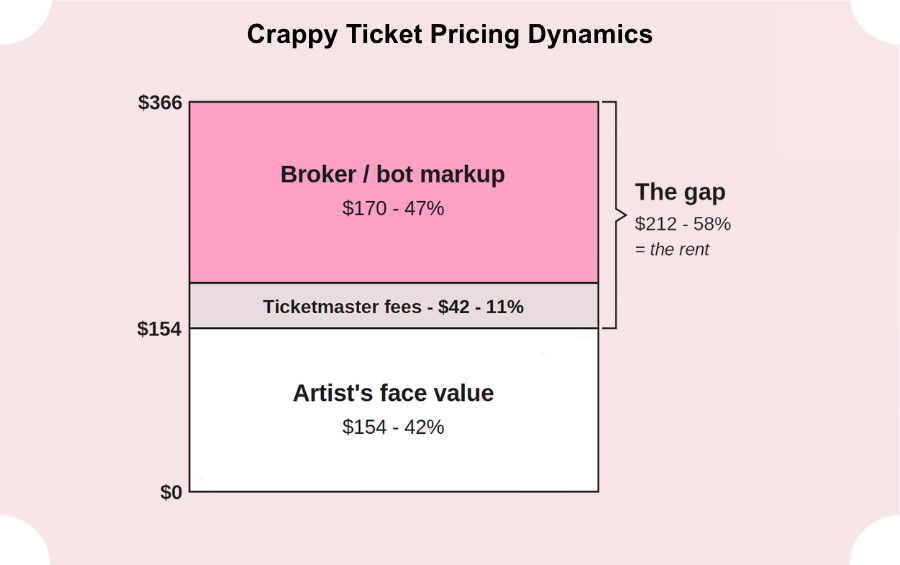

Consider the Eras Tour. When tickets went on sale in November 2022, Ticketmaster's Verified Fan system collapsed under demand, but Capital One — the tour's official presenting partner — had carved out an exclusive presale allocation for its Venture X cardholders, who could entered a promo code and buy at face value, which ranged from $49 to $499. Everyone else fought bots, waited in queues that stalled for hours, and ultimately turned to StubHub, where average tickets resold for thousands — the difference captured by what Ticketmaster euphemistically calls "dynamic pricing," the polite term for the practice of extracting, in real time, the difference between what an artist who wants to keep faith with her fans is willing to charge and what the most liquid fans are willing to pay [4].

The system, which rewards middlemen creating zero value, stiffs artists, and punishes fans, remains in place. The Justice Department's 2024 antitrust suit against Live Nation, joined by 30 state attorneys general, quotes Live Nation executives describing their own venue contracts as "fucking crazy" leverage. JPMorgan Chase has underwritten Live Nation's bond issuances for years.

The card system works because one defining feature of the upper-middle class is a refusal to accept the (likely) permanence and importance of its socio-economic position. Christopher Lasch, in 1979's The Culture of Narcissism, called the professional class "incapable of sustained commitment to any collective purpose larger than its own well-being." Sartre used the term “seriality” to describe people aggregated by a shared bond with an institution rather than shared bonds with each other. A series becomes a group when its members start talking to each other — the one perk Chase and Amex don't prioritize. There's a reason the most notable example of upper-middle class mutualism emerged from army officers whose entire profession was the practice of coordinated movement.

Cardholders don't see themselves as a class — much less a group or collective — so they end up on a list. Members of the Oat Milk Elite love to be on the list even though no list-based system really serves their best interests.

None of which is to say that upper-middle mutualist societies don't exist. REI, a 501(c)(12) consumer co-op remains popular despite the CEO having to step down in 2024 after trying to break a union push (not a great look). Members pay a $20 lifetime fee and dividends ("the divi") are distributed annually. Still, there are caveats: Members don't elect the board, and the cash redemption option was eliminated in 2022, so dividends are discounts in drag. Costco is similar. But neither brand is ultimately antagonistic to vendors. They are convenient, not coercive, which is why the government isn’t attempting to intercede – as it did in 1914 when it failed to break up A&N's American cousin Sears Roebuck.

Lack of pushback is a sure sign no one is pushing too hard and a strong indication that mutualism has been replaced by quasi-mutualism – listism, if you will.

Unlike lists, real mutualism is powerful. Though it feels absolutely ridiculous to mention in the same article as a wine-buying scheme, the Montgomery bus boycott is the ur-example of the power of collectivized consumers. In 1955, fifty thousand Black residents of Montgomery, Alabama, ran a 381-day boycott of the city's bus system over a pricing-and-access structure the city refused to address. Rosa Parks refused to give up her seat on December 1, 1955. The boycott began four days later and on December 20, 1956, after 381 days, the Supreme Court ruled in Browder v. Gayle that bus segregation was unconstitutional. Montgomery City Lines integrated the following morning.

A cardholder being waved into the Sapphire Lounge at LaGuardia likely has very little in common with Rosa Parks, but that doesn't mean he or she shouldn't try to think like her — to adopt her belief that broken, immoral systems can be fixed through collective action.

British Army officers in 1871 were paying too much for claret and decided to fix the system. Platinum cardholders in 2026 are paying too much for everything and we’ve decidedto fix nothing. An invitation to a tasting event-slash-concert in Napa is nice — it feels good to be on the list — but it doesn't change the price of chardonnay. |