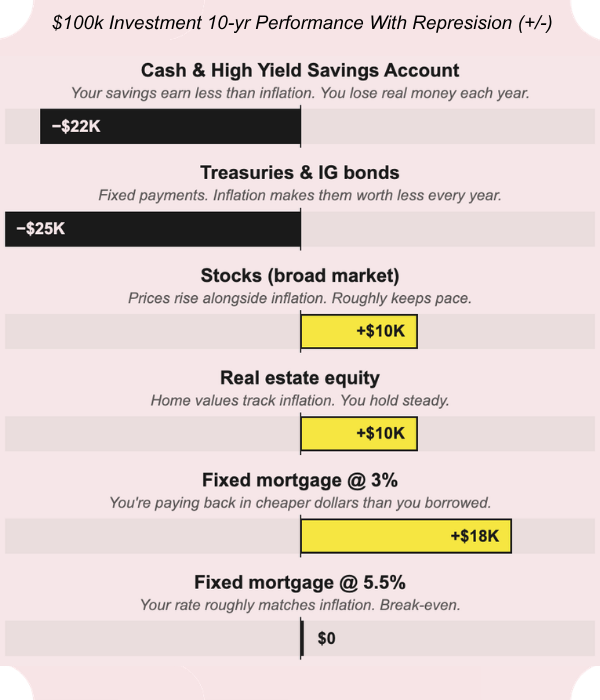

Macro-finance YouTube is melting down because presumptive Fed Chair Kevin Warsh did not explicitly reject the possibility of "financial repression" in his Senate hearings. The most bobbliest of the talking heads are claiming retail investors need to move their money by May 15th, when Powell's term as Fed chair ends. That's nuts, but concern (or just awareness) is warranted. Financial repression means holding interest rates below inflation so bondholders lose some purchasing power every year and the government's debt shrinks at the same rate. (Think: a restaurant that shrinks the by-the-glass pour while still selling full bottles.) It's how the U.S. retired its WWII debt; 106% of GDP in 1946, 23% by 1974. Carmen Reinhart and Belen Sbrancia laid out the playbook in The Liquidation of Government Debt, a 2015 IMF paper. Debt market trends suggest many believe Warsh — Morgan Stanley alum, Bilderberg attendee — is ready to call that audible.

Public and private debt are linked; when the government runs up a debt, the private sector usually has a surplus and vice versa. Historically, that private debt is held – or experienced as a decline in purchasing power – by those least able to push back. Repression hits savers with cash, bonds, and CDs while benefiting those with fixed-rate mortgages, business loans, and other long-dated debt — which is to say homeowners with big mortgages, leveraged real estate investors, private equity bros, and the debt-happy rich. The upper-middle class is the only group whose outcome depends on which side of the financial fence they sit on. Many of us sit precisely on said fence – uncomfortable, sure, but less so if we can just relax.